Achieve net-zero Scope 2 emissions by the end of 2025

Our Products and Climate Change

We are focused on supplying the critical resources needed to build a low-carbon future, including focusing on copper growth.

Our ambition is to achieve net-zero greenhouse gas (GHG) emissions by 2050 across all aspects of our business and activities.

In 2024, we released our Climate Change and Nature Report, which for the first time incorporates the recommendations of the Taskforce on Nature-related Financial Disclosures (TNFD) and the Taskforce on Climate-related Financial Disclosures (TCFD). This report details how we are integrating nature and climate considerations into our strategy as we work to build Teck into one of the world’s leading providers of responsibly produced energy transition metals.

NET-ZERO SCOPE 2

Achieve net-zero Scope 2 emissions by the end of 2025

OUR OPERATIONS

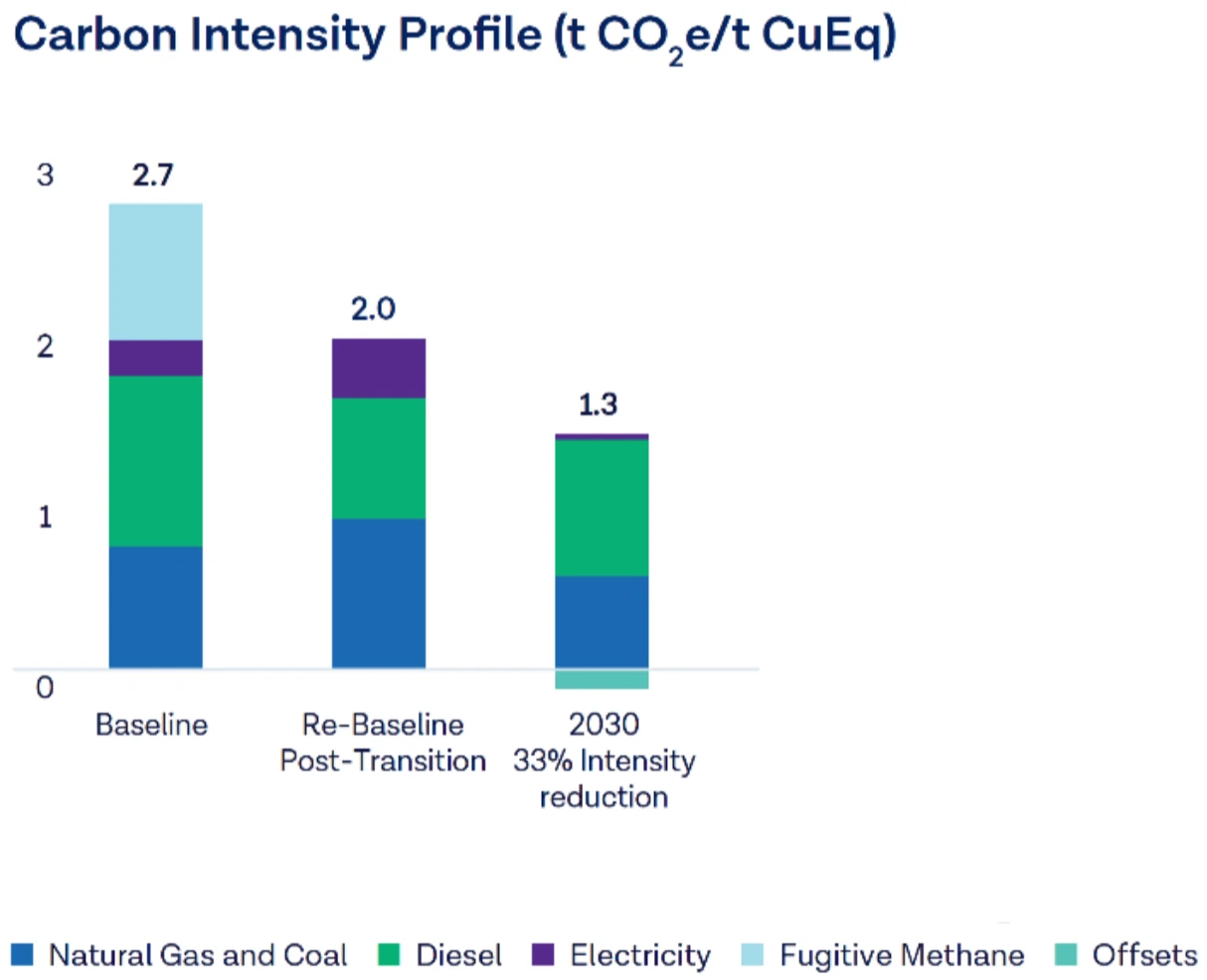

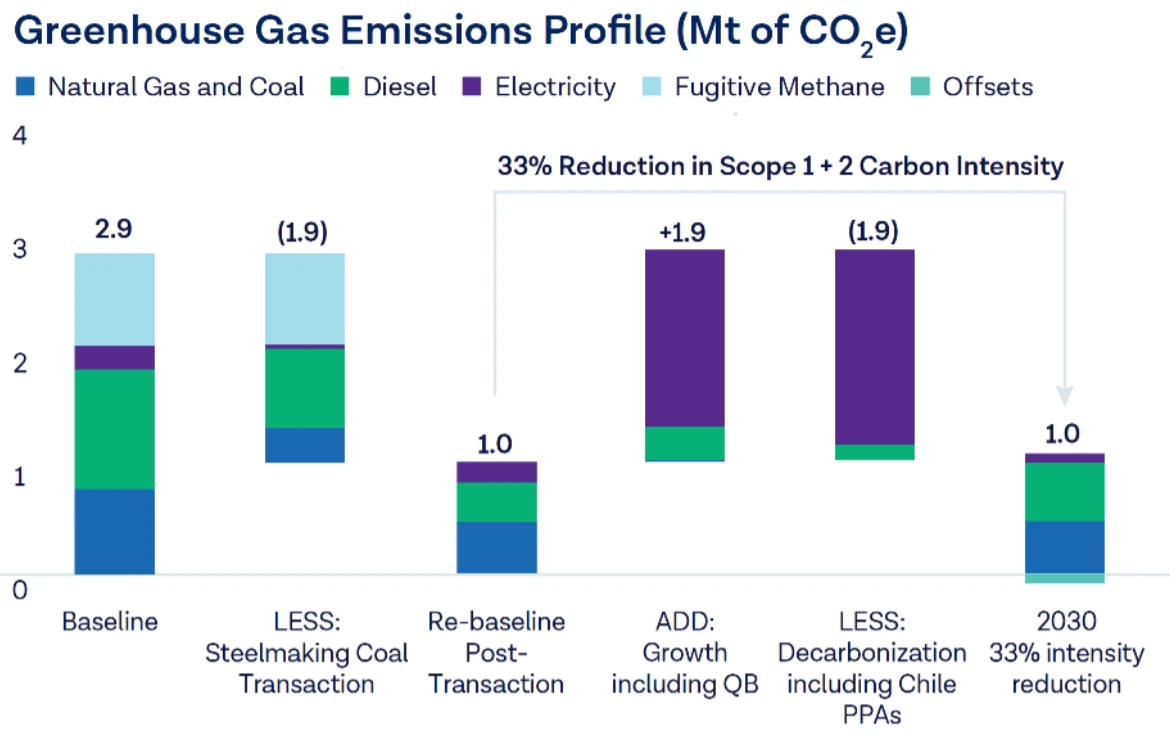

Reduce the carbon intensity of our operations by 33% by the end of 2030, compared to a 2020 baseline

Establish low-emission supply chain corridors, including support for a 40% reduction in shipping emission intensity, working with customers and transportation providers.

*Based on 2020 baseline.

NET-ZERO EMISSIONS

Achieve net zero greenhouse gas (GHG) emissions across our operations by 2050

Ambition to achieve net-zero Scope 3 emissions.

Following the sale of our steelmaking coal assets, we have restated the 2020 emissions baseline for our 2030 goal to reflect the appropriate scope of operations and emissions within our portfolio. This approach to rebaselining is in line with the GHG Protocol’s A Corporate Accounting and Reporting Standard.

To achieve net-zero GHG emissions across our operations and throughout our supply chain, we will implement a range of abatement options including renewable energy use, biofuels, carbon offsets, and more.

We are evaluating and monitoring a wide range of technologies and implementing emissions reductions solutions to reduce our future cost exposure to increasing carbon taxes and other climate-related risks. Our evaluations include technical and financial considerations and are ranked based on their marginal abatement costs. This approach facilitates the prioritization of options that are the most cost-effective, while balancing cost efficiency with commercial, technological, and execution risk.

More details on our decarbonization efforts can be found here.

Scope 1 and 2 Emissions

Operational GHG emissions, which include emissions from energy sources owned and operated by Teck and emissions related to the generation of purchased electricity used by Teck.

Scope 3 Emissions

GHG emissions from sources owned or controlled by other entities downstream of our value chain including the transportation and use of our products.

This document outlines the boundaries, calculation rationale, methodology and assumptions of Teck’s Scope 1, 2 and 3 GHG emissions inventory for the 2023 reporting year.

Our report on our 2022 emissions inventory can be found here.

We aim to contribute to a low-carbon future by producing essential metals and minerals, reducing our carbon footprint, advocating for climate action, and strengthening our resiliency to climate risks. Learn more about our climate strategy.

.png)

Teck is one of the world’s lowest-carbon intensity miners for copper, and zinc. Our management approach, annual performance and data related to climate change can be found below.

.png)